During the third episode (Plan Recovery) of the International Air Transport Association (IATA) webinar, different guests (CEOs, Directors and Experts of companies related to aviation) participated talking about different recovery plans and discussed about the relevance of data analysis for airlines in the worst period in the history for aviation.

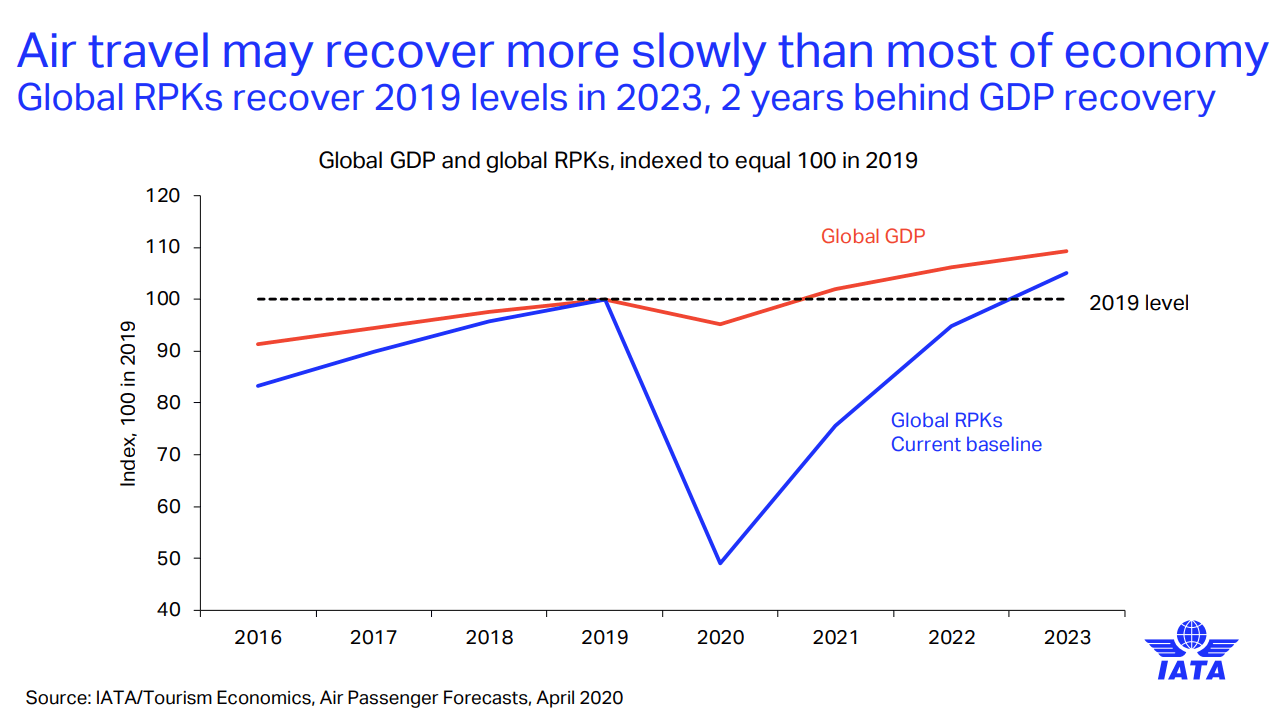

Observing these slides, the Global GDP will reach the 2019 level during 2021 but the Global RPKs (Revenue passenger kilometres) will reach the 2019 level only in early 2023. Clearly air traffic will have a slower recovery than most of economy as Brian Pierce[1] commented. This is strictly correlated to the Governments will because the resume of domestic flights will be the first move for recovery from countries and after that borders will be opened. A direct comparison of Domestic RPKs and International RPKs let us know better the prediction about recovery in the next years.

Obviously, the lowest point has been reached this year for both indicators but the domestic one will recover first as written before.

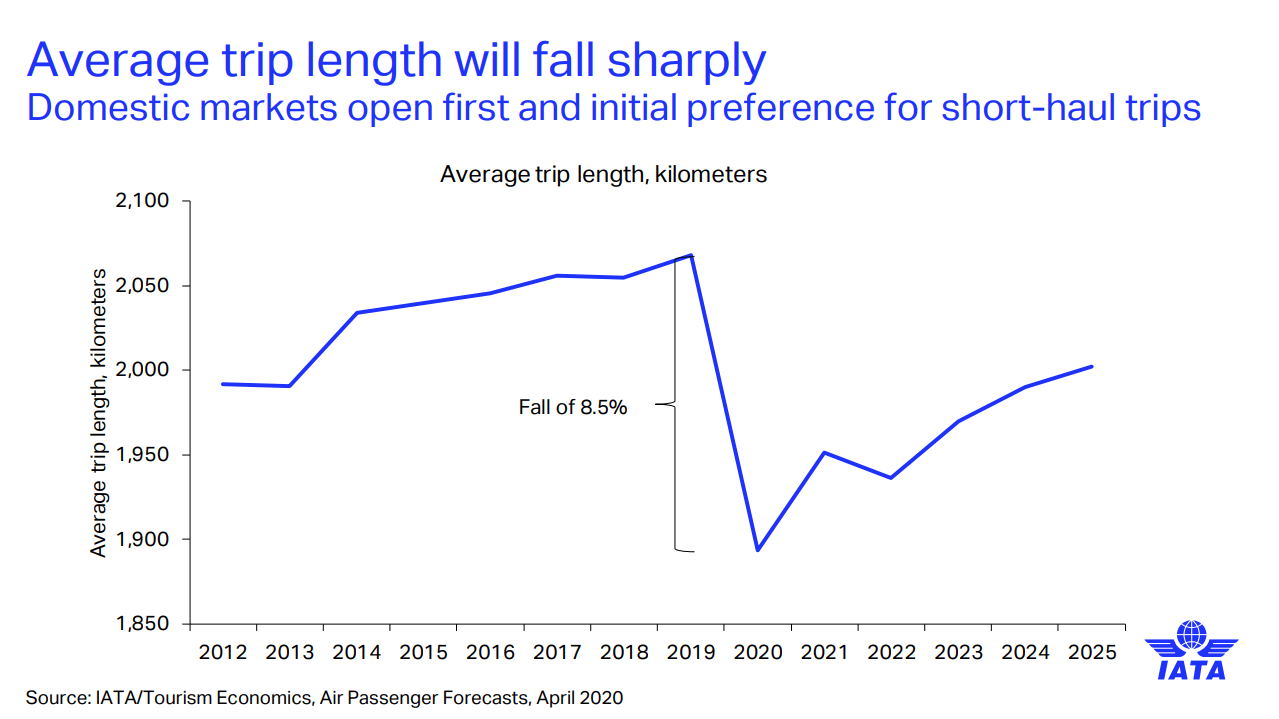

We can demonstrate that by watching at this chart in which the average trip length reached in 2019 will be recovered very slowly in 2025. During the first months immediately after lockdown measures, people might be more confident flying near “home” instead of flying across different continents or even States.

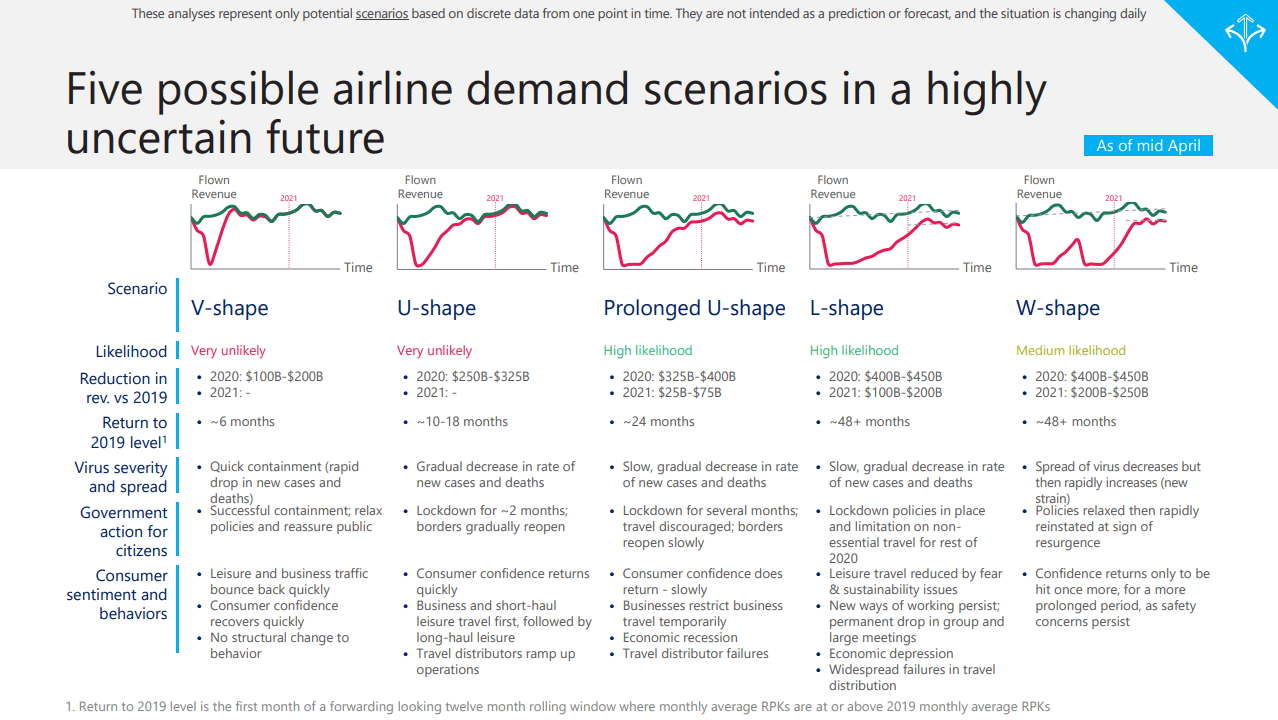

From the perspective of one of the largest airlines in the world, we should look at the way by which they are going to act. Frederik van Essen[2] shows five possible demand scenarios for recovery after the COVID-19 outbreak. The highest likelihood is the “Prolonged U-shape” (third from left). This means that the return to 2019 level will come in 24 months (prediction) while Governments discourage travels abroad and borders would be reopened slowly. As the chart shows, the Prolonged U-shape represents the most gradual recover instead of other scenarios which predict fast recover (6 months for the V-shape for instance). A slow recover, in contrast, involves a “major” reduction in revenues in a range of $325B-$400B in 2020 and $25B-$75B in 2021 compared to the other scenarios as the table below reports.

For an airline, there are two key questions:

- What will be the duration of crisis?

- What will be the shape of recovery?

For both questions, the key indicators to track are COVID-19 development and – consequently – predictions about when travel restrictions between countries will be lifted.

Collecting data will be one of the key for the recovery since airlines have to reset and resize network and fleet by looking at expected demand recovery and different market scenarios besides optimizing for free cash flows or profit since liquidity lack represents the most common problem that airlines are struggling with during this crisis. For this reason, airlines now must rely – more than ever – on data. These are usually collected by companies (e.g. OAG, Infare, ForwardKeys, winglet.io etc.) to know customer preferences in order to track demand rebound and to plan recovery (at least in the short term) building a solid and efficient structure of schedule.

Nina Wittkamp[3] summarizes a selection of leading indicator for air travel demand rebound as recovery scorecard with an overview of leading indicators, demand and capacity trends, sentiment and Web Analytics dashboard to know travel interests (using Google search trends as a proxy), searches and bookings by country and their corresponding trends and air travel capacity compared to current air travel demand and supply.

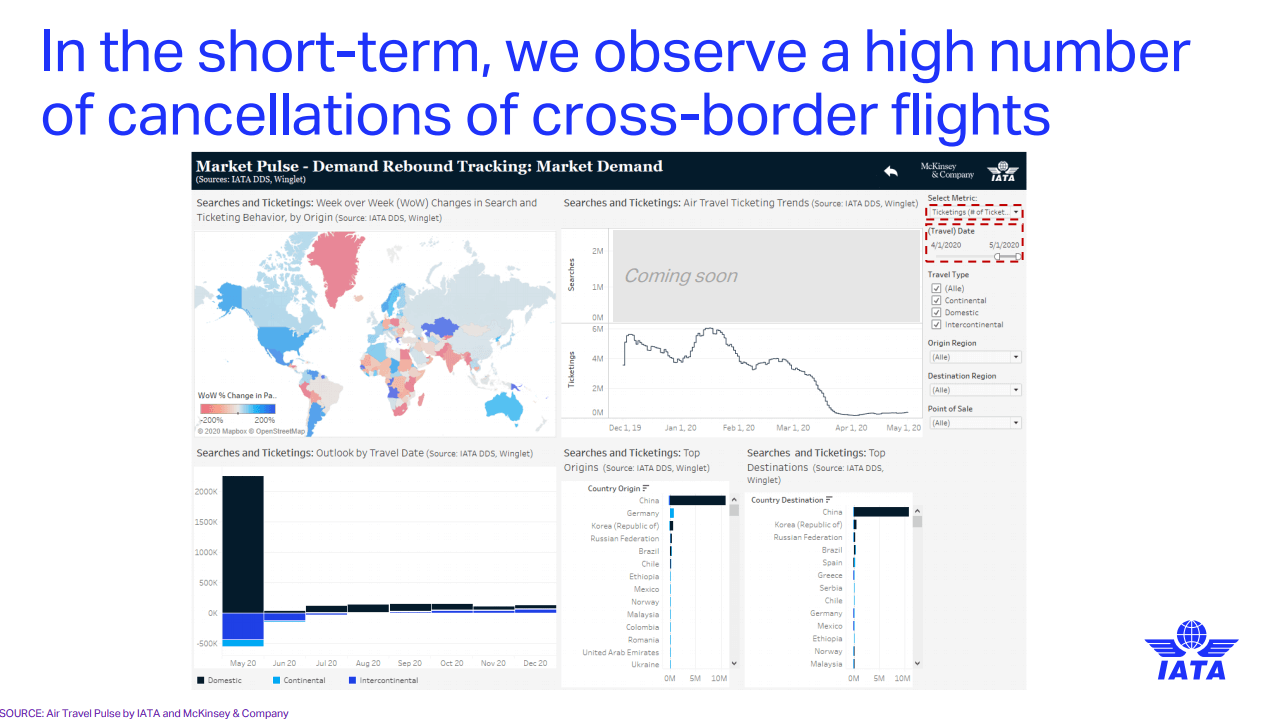

In the short term, the number of cancellations of cross-borders flights is high as we can see from the second chart in the following slide “Air Travel Ticketing Trends”. The line sharply falls starting from the end of March being constant until now observing a slow increase during these last days. In the third chart, “Outlook by travel date”, we can find a confirmation of the data written in first paragraph: domestic flights have a “preferred” outlook than continental and intercontinental flights for the next months to come. August represents better this situation in which there are zero searches and ticketings for abroad travels.

[1] Chief Economist at IATA

[2] Commercial Director, Digital Operation, KLM

[3] Expert Associate Partner, McKinsey & Company