Partner content | As air traffic volumes and aeronautical revenue streams dry up, airports find themselves under increasing credit stress. Julyana Yokota, Senior Director, Infrastructure, at S&P Global Ratings, examines the long-term outlook for airports’ recovery.

Government-imposed lockdowns across the globe have precipitated an unprecedented decline in air traffic, while the resultant economic crisis has brought with it significant credit stress across markets. As a result, S&P Global Ratings anticipates a deep recession in 2020, with GDP set to contract by 7.8% in the EU and 5% in the US. Of all the infrastructure asset classes, aviation is a strong contender for the worst hit by the pandemic, with COVID-19 expected to have a more prolonged effect on the sector than previous large-scale disruptions such as 9/11 and the financial crisis of 2008-09.

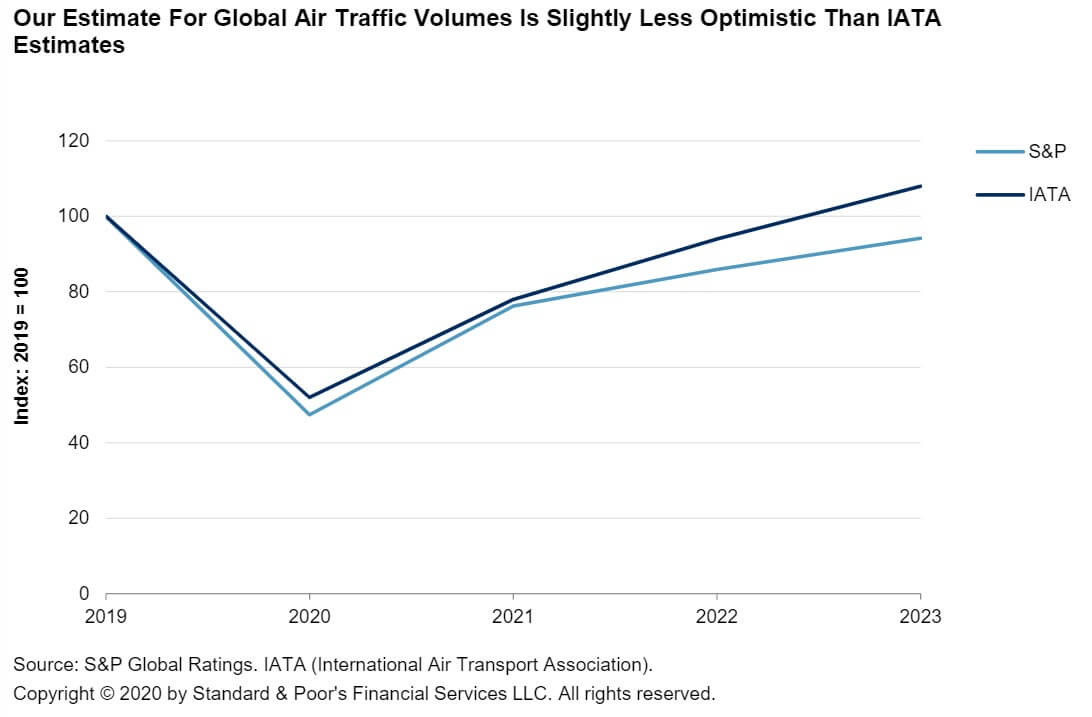

Indeed, S&P considers COVID-19 to have outsized impact even when compared to previous pandemics such as SARS in 2003. We estimate that global passenger air traffic will decline by between 50% and 55% in 2020, taking into account the almost three months in which traffic dropped below 90% compared with the same period the previous year.

The drop in global traffic volumes is to be followed by a slow climb back to pre-pandemic levels – a phenomenon which we have termed a ‘swoosh-shaped’ recovery. Our recovery estimates are broadly aligned with those of the International Air Transport Association (IATA) for 2020 and 2021, however we are somewhat less optimistic about the time it will take for traffic levels to return to pre-pandemic levels and anticipate this could stretch through 2023 due to limited foresight on future consumer behaviours.

Testing times

Airports generally enjoy stronger liquidity positions than airlines, however as a result of the downturn are facing significant credit implications – especially as aeronautical revenue dries up and airports are left to finance both operations and debt acquired in the recent boom years. Certainly, airports have significant levels of fixed costs, and many have had to remain open to serve repatriation and cargo flights.

While major national airports – especially those in Europe – are likely to maintain an adequate level of financing, many are in desperate need of government support which, to date, has mostly been directed towards airlines. Our recent ratings reflect these growing levels of credit stress: between March and June 2020, S&P lowered its ratings on 12 airports, the bulk of which were one notch downgrades – especially in Europe and the U.S. However, in Latin America, we have witnessed a more severe downside, with Aeropuertos Argentina 2000 S.A. defaulting through a distressed debt exchange.

In addition to credit concerns, a weakened airline sector is certain to have a knock-on effect on airports. Indeed, post-pandemic, airlines are likely to be fewer in number owing to potential consolidations and bankruptcies – as seen in the case of Flybe and Avianca (AVHOQ) . Those that do survive will be financially weaker and will apply downward pressure on aviation charges – a key component of airport revenue. Single-till regulatory regimes have provisions for charges to be revised in the face of drops in traffic volumes, but in these unprecedented circumstances airlines may have more of a hand in dictating charges than their regulatory counterparts.

With aeronautical revenues set to remain lower for the foreseeable future, airports must therefore make an effort to diversify their revenue streams. One strategic avenue operators can explore is office real estate. Another option is expanding into online retail – something that would become a more attractive proposition if social distancing continues to factor into consumer behaviour in the longer term.

Adjusting to the new normal

For the time being, it appears that the peak of the pandemic has passed. Many governments are gradually re-opening borders and tourism is set to return through ‘corridors’ between relatively safe areas. Of course, a much feared second wave of the virus could materialise, but current assumptions are that this is likely to be more localised than the initial outbreak. Nevertheless, such a large-scale disruption has changed consumer attitudes towards air travel.

Moving forward, airports will have to reckon with a number of significant changes as they adjust to the ‘new normal’. Some level of structural change in the aviation sector is inevitable – especially as governments are likely to be prudent when removing restrictions on borders. In the shorter term, this will likely mean social distancing measures remain in place, in turn leading to less busy airports and reduced seating occupancy on-board. Yet the extent of longer-term behavioural changes – such as an avoidance of air travel or a reduction in business trips following the adjustment to remote meetings – remain to be seen.

Despite this, we do not expect the airport industry to face secular change. Tourism supports one in 10 jobs globally, and commercial air travel will remain the fastest, most affordable way to move people across long distances. What’s more, pre-pandemic levels of yearly air traffic growth – which stood at 4%-5% – support a return to some level of normality. Therefore, while airports certainly face turbulence in the short-to-mid-term, their infrastructural significance as an essential gateway to a globalised world remains unchanged.