After a disappointing 2021, where a hoped-for recovery stalled, airport operators are looking forward to better times as 2022 has started to indicate improved conditions for the hard-hit sector, Nishant Mishra, Associate Director at Acuity Knowledge Partners writes in an exclusive piece for AeroTime.

Green shoots of recovery in 2022

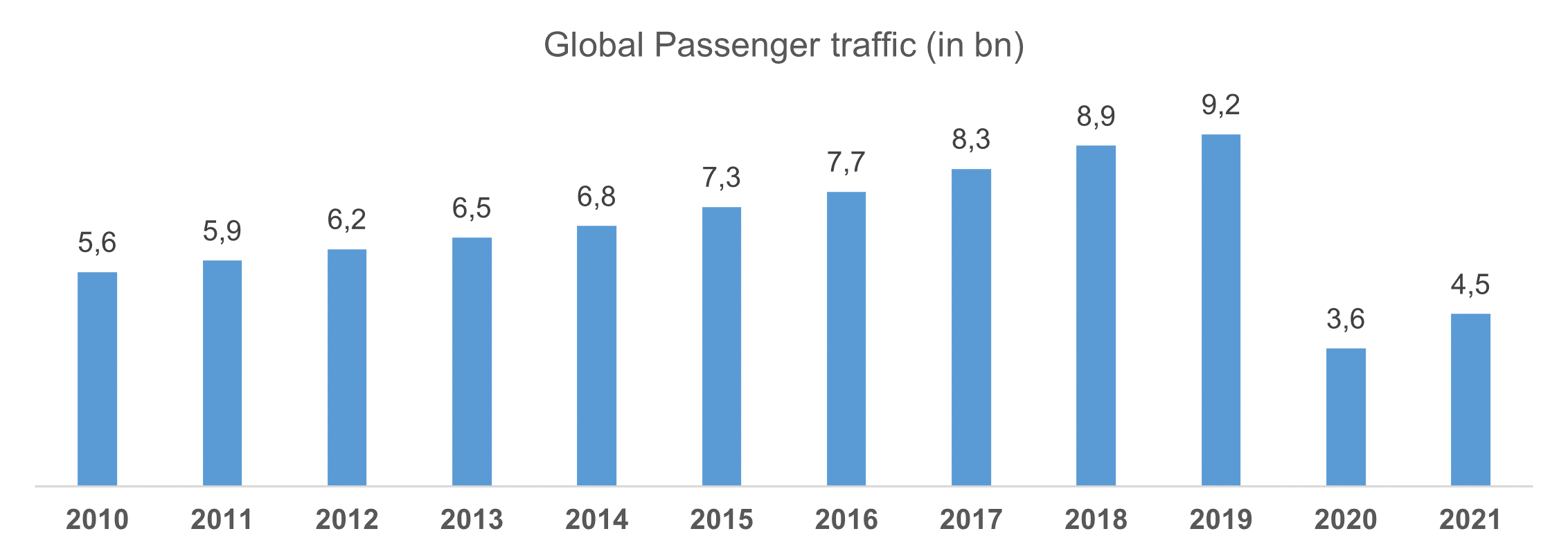

After a disappointing 2021 where a hoped-for recovery stalled, airport operators are looking forward to better times as 2022 has begun to indicate improved conditions for the hard-hit sector. According to the Airports Council International (ACI), the leading representative body for the world’s airports, passenger traffic increased 25% year-on-year (y/y) in 2021 to 4.5 billion globally. But it remained 51% below 2019 levels.

Traffic up 25% y/y in 2021 but down 51% vs 2019. Source: ACI

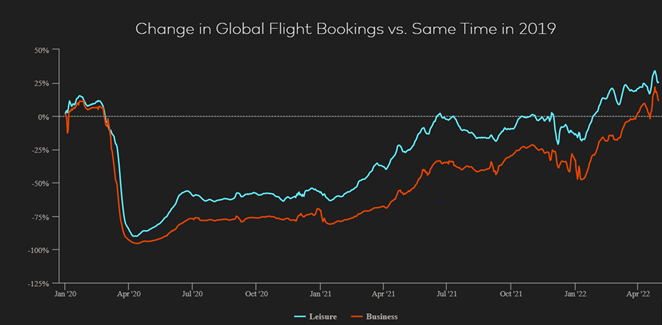

For 2022 and beyond, the outlook for the airports sector is positive as the large-scale roll-out of vaccination programs globally (c.60% achieved in most geographies by end-1Q22) has helped to slow the spread of COVID, and the air travel and tourism industries have resumed their upward climb. Leisure bookings for summer (June to August, traditionally the busiest and most profitable season) have already surpassed 2019 levels and will likely propel the expected 2022 recovery. Aided by the easing international travel restrictions, corporate travel is improving faster than expected, touching the highest level since the pandemic began.

Globally, short-haul business travel witnessed strong growth in April and surpassed 2019 levels by 24%. In the coming months, we will also see a strong recovery in the medium-and long-haul markets which were down 5% and 8% respectively below pre-pandemic levels.

Leisure and corporate booking higher than the Pre-Pandemic level. Source: Mastercard Economics Institute

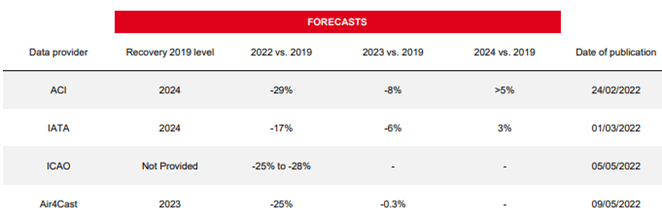

We expect that airports with a higher mix of domestic traffic will recover faster versus international hubs, which will take a little longer. The positive indicators seen in 2022 thus far should be set in the wider context of the sector’s long journey towards pre-pandemic volumes. The major data providers covering the sector do not see such a full recovery occurring until 2024 at the earliest.

Global air travel passenger recovery only by 2024. Source: Dufry

Airlines shifting strategic focus from capex (towards capacity growth) to optimization (improving utilization)

Part of the challenge which airports will grapple with between now and 2024 is the correlation between their revenues and those of the airlines they serve. Airlines themselves are dealing with the financial legacy of the pandemic – airline industry losses are expected to reach $US11.6 billion in 2022 (vs. $US51.8 billion in 2021) with cumulative losses of $US201 billion from 2020-2022. An industry which once focused on expanding capacity has shifted its strategy to achieving higher yields by optimizing load factors by enforcing considerable capacity discipline. This is chiefly driven by lower traffic growth and significant fuel price concerns.

The industry has witnessed escalating consolidation, bankruptcies and unprofitable route cuts in many mid-size and small markets, as well as mergers as part of global alliances. Capacity reduction now matters less to airlines, as they are entering into alliances and Joint Ventures (JVs) to share profit and cooperate on schedules. As a result, many airports have witnessed fewer services from airlines. Airports that have a hub carrier or a dominant airline (which accounts for greater than 40% of the airport’s capacity) are highly reliant on the airline’s future capacity plans and could be severely impacted by any cuts in capacity plans due to staff shortages and rising fuel prices, as well as aircraft delivery delays (for example British Airways recently announced its plans to cut capacity by 5% over the summer due to a lack of staff – this will have a big impact on Heathrow airport).

Currently, both full-service carriers and low-cost carriers (LCCs) practice similar capacity discipline, leaving some small and medium-sized hub airports incapacitated to challenge their bigger, nearby rivals on price or service. Moreover, LCCs’ rapidly expanded share (35% of the global air travel market) poses a threat to airports as LCCs are cost-focused and employ a more flexible model for deploying aircraft in response to dynamic profit opportunities.

Increase in airport charges inevitable, but airlines plan to push back

In the last two years, airports have delayed the planned increase in aeronautical charges (their major revenue generator at 50-60% of total revenue). Some airports have even provided relief to airlines, partially waiving the charges. However, going forward, we expect airports to steadily raise the charges to repay and service their mounting debt. They may tweak the charges (expected to continue over the next five to seven-year period) to recover their 2020 and 2021 losses. Recently, Amsterdam Schiphol Airport (72 million passengers in 2019) has been given permission by the Dutch regulator to apply a 37% hike in airport charges over the next three years.

Non-aeronautical revenue slowly picking up while cargo traffic provides a lifeline

Non-aeronautical revenue, which accounts for 35-40% of total airport revenue, has started recovering slowly as many retail outlets and duty-free shops have resumed operations with a limited capacity. However, encouraging travel demand and continued easing of travel restrictions offer a ray of hope to airport retailers. Dufry, the world’s biggest airport retailer, has now re-opened around 85% of its shops globally (greater than 90% of its sales capacity). It reported organic net sales growth of 144.5% y/y in 1Q22 and estimates April 2022 organic growth at 176.2% (vs 2021).

Cargo revenue, which witnessed record growth at the peak of the pandemic, is expected to remain robust in 2022 (IATA estimates 13% growth in demand in 2022 vs 2019). This was mainly due to a rise in e-commerce demand across regions and the need for effective air freight to support global supply chains. Belly cargo (transportation of goods via passenger aircraft) is also picking up as airlines resume more flights and increase capacity. Nevertheless, it will take time to recover to its pre-pandemic levels.

Airports’ credit profiles are improving

Most rated airports are investment-grade. Currently, rating agencies have placed a stable to negative outlook on their existing rating given the uncertainties surrounding traffic recovery (full recovery expected by 2024). However, their prospects are improving with most airports recording high treble-digit y/y traffic growth rates in Q1 2022 (for example, Heathrow +575%, Dubai +239%, and Paris +230%).

Nonetheless, the credit profile of airports hinges on significant government back-up in terms of capital injections and other programs (such as the Airport Rescue Grant). The impact of the Russia-Ukraine conflict is likely to be minimal overall and only a few countries’ airports, including Finland, Estonia, Germany, and Italy, will be impacted, which are among the top 10 international destinations for Russian tourists. However, the negative impact on Russian airports is likely to be material, due to the international sanctions (Russian aviation blog).

Fixed costs make up a large share of airports’ costs, not surprising for capital-intensive businesses. Notwithstanding the lower scale of operations (attributable to terminal closure, layoffs etc.), almost all airports are operating at a loss. Airports have drastically cut operating expenditure (OpEx) and deferred growth (CapEx) to remain afloat, aided by surplus current capacity to cater to the demand for the next couple of years before airports recover fully.

Moreover, given airports’ systemic importance in the economy, governments and other stakeholders (including creditors which have already waived/are planning to waive financial covenants) will likely continue their strong support. Also, given the elevated fuel costs and stretched balance sheets, the potential bankruptcy of unhedged/weaker airlines with a substantial stake in airport operations is a key concern.

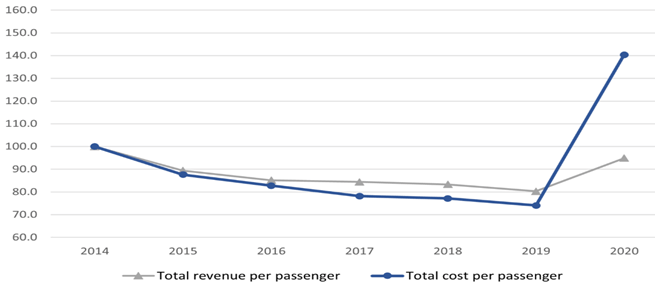

Evolution of unit revenues and costs per passengers (2014–2020, indexed 2014=100). Source: ACI World Economic dataset

Airports with a high proportion of international traffic are expected to recover more slowly due to continuing travel restrictions in two key markets: the US (which permits only fully vaccinated flyers to travel) and China (which is still pursuing its zero-COVID-19 policy and has imposed strict restrictions). However, governments worldwide are unlocking travel restrictions to prop up travel, tourism and trade. ACI believes that the COVID-19 pandemic will continue to erode airports’ revenue in 2022, which will likely shrink an additional $US60.8 billion and stand at 72.6% of 2019 revenue. In our view, revenue losses will likely continue in 2023 in the sector.

We believe the strong growth in passenger traffic in recent months will likely sustain due to high levels of vaccination, easing mobility restrictions and pent-up travel demand. This, together with the expected increase in airport charges, hints at easing fiscal strains, positioning airports to return to profitability. This, in turn, will likely ratchet up its ability to achieve credit metrics commensurate with its existing ratings by 2024. Also, many airports successfully entered the market in 2022 through increased debt issuances, which also signals a return to normalcy. However, the material impact of any new COVID-19-related lockdowns or an escalation of the Russia-Ukraine conflict could prolong airports’ woes until 2025, which is something that investors will need to bear in mind.

About the author. Nishant Mishra, Associate Director at Acuity Knowledge Partners, has close to 18 years of work experience in investment research, including 14 years at Acuity Knowledge Partners, with a focus on the transportation, utilities, capital goods and energy sectors. With expertise in both equity and fixed income research, he currently leads teams that provide research support to European buy- and sell-side clients. The work involves building detailed financial models, distressed debt analysis, writing initiation reports and assisting clients with investment decisions for investment-grade, high-yield and distressed-debt companies in developed and emerging markets. He acts as a single point of contact for clients and ensures the team delivers high-quality output in line with SLAs. He holds a Master of Business Administration (Finance) and a Bachelor of Business Administration.